Home /

Expert Answers /

Accounting /

sierra-company-manufactures-soccer-balls-in-two-sequential-processes-cutting-and-stitching-all-d-pa971

(Solved): Sierra Company manufactures soccer balls in two sequential processes: Cutting and Stitching. All d ...

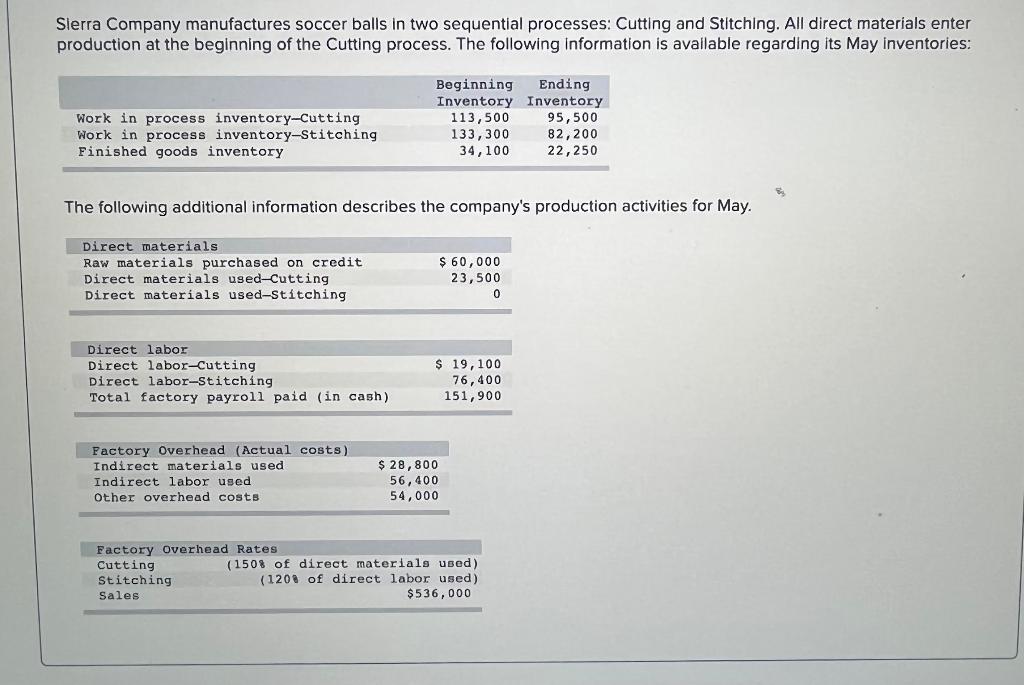

Sierra Company manufactures soccer balls in two sequential processes: Cutting and Stitching. All direct materials enter production at the beginning of the Cutting process. The following information is available regarding its May inventories: Work in process inventory-Cutting Work in process inventory-Stitching Finished goods inventory The following additional information describes the company's production activities for May. Direct materials Raw materials purchased on credit Direct materials used-Cutting Direct materials used-Stitching Direct labor Direct labor-Cutting Direct labor-Stitching Total factory payroll paid (in cash) Factory Overhead (Actual costs) Indirect materials used. Indirect labor used Other overhead costs. Beginning Ending Inventory Inventory 113,500. 95,500 133,300 82,200 34,100 22,250 Factory Overhead Rates Cutting Stitching Sales $ 60,000 23,500 0 $ 19,100 76,400 151,900 $ 28,800 56,400 54,000 (1508 of direct materials used) (120 of direct labor used) $536,000

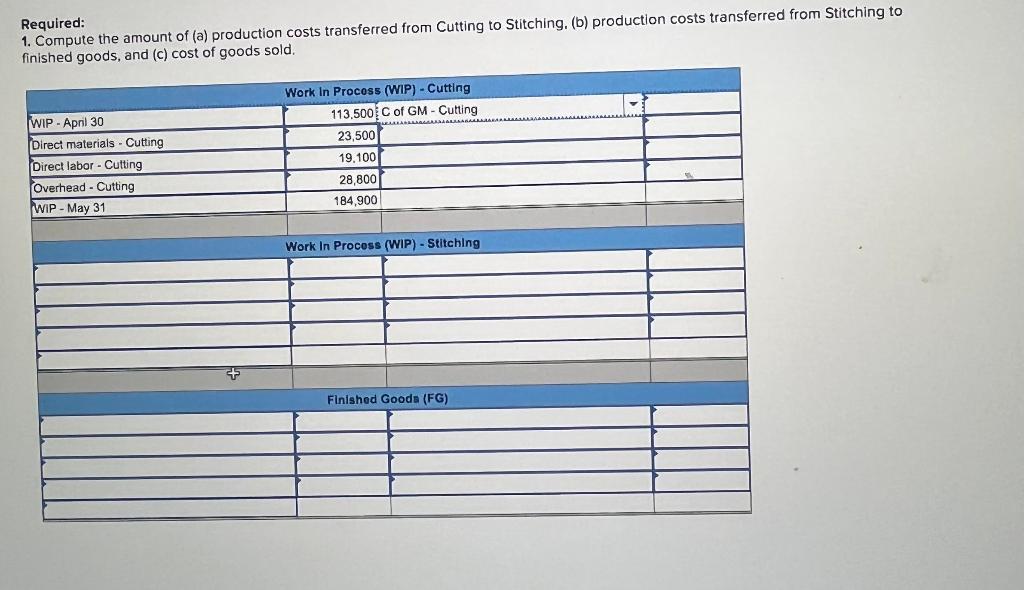

Required: 1. Compute the amount of (a) production costs transferred from Cutting to Stitching, (b) production costs transferred from Stitching to finished goods, and (c) cost of goods sold. WIP - April 30 Direct materials - Cutting Direct labor Cutting Overhead - Cutting WIP-May 31 Work In Process (WIP) - Cutting 113.500 C of GM - Cutting 23,500 19.100 28,800 184,900 Work In Process (WIP) - Stitching Finished Goods (FG)

Expert Answer

Answer: 1) (a) Production costs transferred from cutting to stitching $ 95850 (b) Production costs transferred from stitching to finished goods $ 31