Note: This problem is for the 2021 tax year.

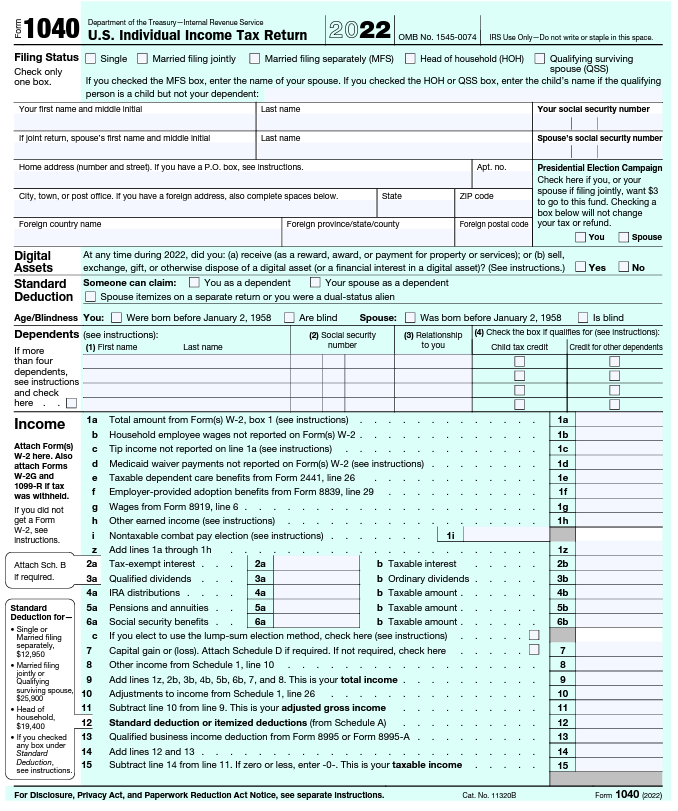

Roberta Santos, age 41, is single and lives at 120 Sanborne Avenue, Springfield, IL 62701. Her Social Security number is 123-45-6780. Roberta has been divorced from her former husband, Wayne, for two years. She has a son, Jason, who is 17, and a daughter, June, who is 18. Jason's Social Security number is 111-11-1112, and June's is 123-45-6788. Roberta has never owned or used any virtual currency. She does not want to contribute $3 to the Presidential Election Campaign Fund. Roberta received the appropriate recovery rebates (economic impact payments); related questions in ProConnect Tax should be ignored.

Roberta, an advertising executive, earned a salary from ABC Advertising of $136,000 in 2021. Her employer withheld $16,000 in Federal income tax and $4,400 in state income tax.

Roberta has legal custody of Jason and June. The divorce decree provides that Roberta is to receive the dependency deductions for the children. Jason lives with his father during summer vacation. Wayne indicates that his expenses for Jason are $5,500. Roberta can document that she spent $8,500 for Jason's support during 2021. In prior years, Roberta gave a signed Form 8332 to Wayne regarding Jason. For 2021, she has decided not to do so. Roberta provides all of June's support.

Roberta's mother died on January 7, 2021. Roberta inherited assets worth $625,000 from her mother. As the sole beneficiary of her mother's life insurance policy, Roberta received insurance proceeds of $300,000. Her mother's cost basis for the life insurance policy was $120,000. Roberta's favorite aunt gave her $13,000 for her birthday in October.

On November 8, 2021, Roberta sells for $22,000 Amber stock that she had purchased for $24,000 from her first cousin, Walt, on December 5, 2016. Walt's cost basis for the stock was $26,000. On December 1, 2021, Roberta sold Falcon stock for $13,500. She had acquired the stock on July 2, 2017, for $8,000.

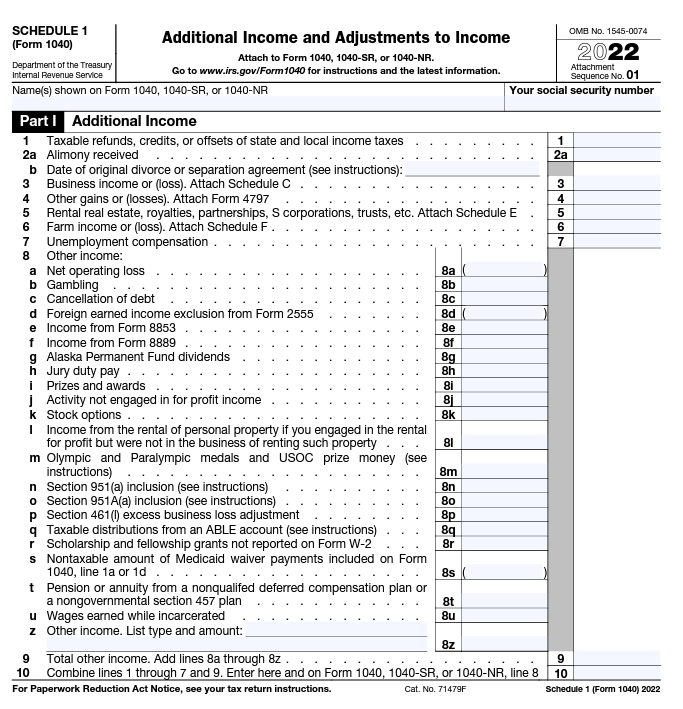

An examination of Roberta's records reveals that she received the following:

Interest income of $2,500 from First Savings Bank.

Groceries valued at $750 from Kroger Groceries for being the 100,000th customer.

Qualified dividend income of $1,800 from Amber.

Interest income of $3,750 on City of Springfield school bonds.

Alimony of $16,000 from Wayne; divorce finalized in May 2019.

Distribution of $4,800 from ST Partnership (Employer Identification Number: 46-4567893). Her distributive share of the partnership passive taxable income was $5,300. She had no prior passive activity losses. Assume that the qualified business income deduction applies and the W–2 wage limitation does not.

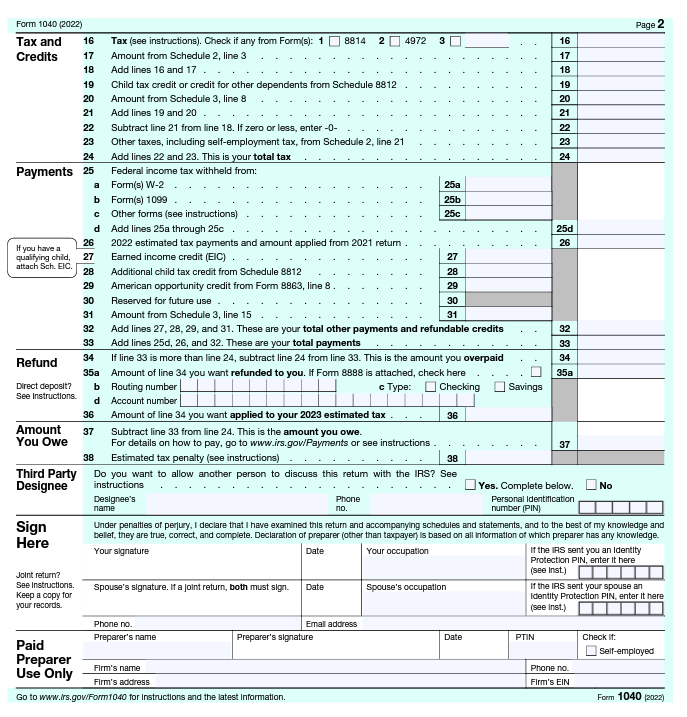

From her checkbook records, she determines that she made the following payments during 2021:

Charitable contributions of $4,500 to First Presbyterian Church and $1,500 to the American Red Cross (proper receipts obtained).

Payment of $5,000 to ECM Hospital for the medical expenses of a friend from work.

Mortgage interest on her residence of $7,800 to Peoples Bank.

Property taxes of $3,200 on her residence and $1,100 (ad valorem) on her car. $800 for landscaping expenses for residence.

Estimated Federal income taxes of $2,800 and estimated state income taxes of $1,000.

Medical expenses of $5,000 for her and $800 for Jason. In December, her medical insurance policy reimbursed $1,500 of her medical expenses. She had full-year health care coverage.

A $1,000 ticket for parking in a handicapped space.

Attorney's fees of $500 associated with unsuccessfully contesting the parking ticket.

Contribution of $250 to the campaign of a candidate for governor.

Because she did not maintain records of the sales tax she paid, she calculates the amount from the sales tax table to be $1,808.

Required:

Calculate Roberta's net tax payable or refund due for 2021.

Enter all amounts as positive numbers. However, use the minus sign to indicate a loss.

If an amount box does not require an entry or the answer is zero, enter "0".

Make realistic assumptions about any missing data.

It may be necessary to complete the tax schedules before completing Form 1040.

When computing the tax liability, do not round your immediate calculations. If required round your final answers to the nearest dollar.

Only use the Tax Rate Schedule provided. Do not use other Tax Tables.

Sign Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and Here bellef, they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Attach to Form 1040, 1040-SR, or 1040-NR.

Schedule 1 (Form 1040) 2022 Page 2 Part II Adjustments to Income

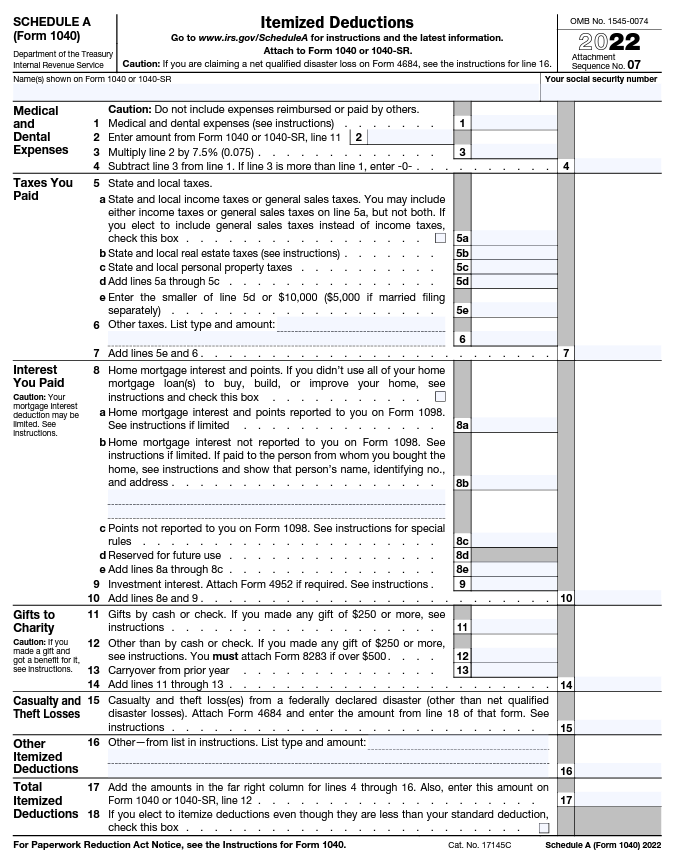

\begin{tabular}{l|c|c|c} SCHEDULE A & Itemized Deductions & OMB No. 1545-0074 \\ (Form 1040) Department of the Treasury Internal Pavenue Service & Go to www.irs.gov/ScheduleA for instructions and the latest information. \\ Attach to Form 1040 or 1040-SR. & 52 \\ \hline \end{tabular} \begin{tabular}{l|l|l|l|l|} \hline Name(s) shown on Form 1040 or 1040-SR & Your soclal security number \\ \hline \end{tabular} Casualty and 15 Casualty and theft loss(es) from a federally declared disaster (other than net qualified Theft Losses disaster losses). Attach Form 4684 and enter the amount from line 18 of that form. See

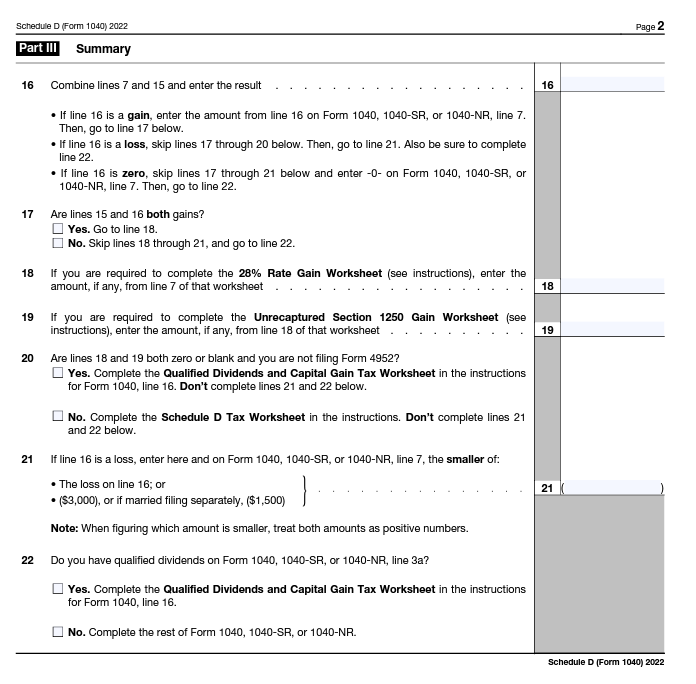

Part II Long-Term Capital Gains and Losses-Generally Assets Held More Than One Year (see instructions)

16 Combine lines 7 and 15 and enter the result - If line 16 is a gain, enter the amount from line 16 on Form 1040, 1040-SR, or 1040-NR, line 7. Then, go to line 17 below. - If line 16 is a loss, skip lines 17 through 20 below. Then, go to line 21 . Also be sure to complete line 22. - If line 16 is zero, skip lines 17 through 21 below and enter -0-on Form 1040, 1040-SR, or 1040-NR, line 7 . Then, go to line 22. 17 Are lines 15 and 16 both gains? Yes. Go to line 18. No. Skip lines 18 through 21 , and go to line 22 . 18 If you are required to complete the \( 28 \% \) Rate Gain Worksheet (see instructions), enter the amount, if any, from line 7 of that worksheet 19 If you are required to complete the Unrecaptured Section 1250 Gain Worksheet (see instructions), enter the amount, if any, from line 18 of that worksheet 20 Are lines 18 and 19 both zero or blank and you are not filing Form \( 4952 ? \) Yes. Complete the Qualified Dividends and Capital Gain Tax Worksheet in the instructions for Form 1040, line 16. Don't complete lines 21 and 22 below. No. Complete the Schedule D Tax Worksheet in the instructions. Don't complete lines 21 and 22 below. 21 If line 16 is a loss, enter here and on Form 1040, 1040-SR, or 1040-NR, line 7, the smaller of: \( \left.\begin{array}{l}\text { - The loss on line } 16 \text {; or } \\ \text { - }(\$ 3,000) \text {, or if married filing separately, }(\$ 1,500)\end{array}\right\} \) Note: When figuring which amount is smaller, treat both amounts as positive numbers. 22 Do you have qualified dividends on Form 1040, 1040-SR, or \( 1040-\mathrm{NR} \), line \( 3 a \) ? Yes. Complete the Qualified Dividends and Capital Gain Tax Worksheet in the instructions for Form 1040, line 16. No. Complete the rest of Form 1040, 1040-SR, or 1040-NR.

Schedule E (Form 1040) 2022 Attachment Sequence No. 13 Page 2 Name(s) shown on return. Do not enter name and soclal securtity nurnber if shown on other side. Your soclal security number Caution: The IRS compares amounts reported on your tax return with amounts shown on Schedule(s) K-1. Part II Income or Loss From Partnerships and S Corporations Note: If you report a loss, receive a distribution, dispose of stock, or receive a loan repayment from an S corporation, you must check the box in column (e) on line 28 and attach the required basis computation. If you report a loss from an at-risk activity for which any amount is not at risk, you must check the box in column (f) on line 28 and attach Form 6198. See instructions. 27 Are you reporting any loss not allowed in a prior year due to the at-risk or basis limitations, a prior year unallowed loss from a passive activity (if that loss was not reported on Form 8582), or unreimbursed partnership expenses? If you answered "Yes," see instructions before completing this section . . . . . . . . . . . . . . . . . . . . . . . . . \( \square \) Yes \( \square \) No 30 Add columns \( (\mathrm{h}) \) and \( (\mathrm{k}) \) of line \( 29 \mathrm{a} \) 31 Add columns \( (\mathrm{g}) \), (i), and (j) of line 29b. 32 Total partnership and S corporation income or (loss). Combine lines 30 and 31 Part III Income or Loss From Estates and Trusts \begin{tabular}{c|} \hline 33 \\ \hline A \\ \hline B \\ \hline \end{tabular} (a) Name (b) Employer Identification number

Schedule 8812 (Form 1040) 2022 Page 2 Part II-A Additional Child Tax Credit for All Filers Caution: If you file Form 2555 , you cannot claim the additional child tax credit. 15 Check this box if you do not want to claim the additional child tax credit. Skip Parts II-A and II-B. Enter -0- on line 27 16a Subtract line 14 from line 12. If zero, stop here; you cannot take the additional child tax credit. Skip Parts II-A and II-B. Enter \( -0 \) - on line 27 b Number of qualifying children under 17 with the required social security number: Enter the result. If zero, stop here; you cannot claim the additional child tax credit. Skip Parts II-A and II-B. Enter -0- on line 27 . TIP: The number of children you use for this line is the same as the number of children you used for line 4. 17 Enter the smaller of line \( 16 \mathrm{a} \) or line \( 16 \mathrm{~b} \). 18a Earned income (see instructions).. b Nontaxable combat pay (see instructions). 19 Is the amount on line 18 a more than \( \$ 2,500 \) ? No. Leave line 19 blank and enter \( -0 \) - on line 20. Yes. Subtract \( \$ 2,500 \) from the amount on line \( 18 a \). Enter the result 20 Multiply the amount on line 19 by \( 15 \%(0.15) \) and enter the result Next. On line \( 16 \mathrm{~b} \), is the amount \( \$ 4,500 \) or more? No. If you are a bona fide resident of Puerto Rico, go to line 21. Otherwise, skip Part II-B and enter the smaller of line 17 or line 20 on line 27. Yes. If line 20 is equal to or more than line 17, skip Part II-B and enter the amount from line 17 on line 27. Otherwise, go to line 21. \begin{tabular}{|l|l|l} Part II-B & Certain Filers Who Have Three or More Qualifying Children and Bona Fide Residents of Puerto Rico \end{tabular} 21 Withheld social security, Medicare, and Additional Medicare taxes from Form(s) W-2, boxes 4 and 6 . If married filing jointly, include your spouse's amounts with yours. If your employer withheld or you paid Additional Medicare Tax or tier 1 RRTA taxes, see 22 Enter the total of the amounts from Schedule 1 (Form 1040), line 15; Schedule 2 (Form 1040), line 5; Schedule 2 (Form 1040), line 6; and Schedule 2 (Form 1040), line 13. 23 Add lines 21 and 22 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . \( 24 \quad 1040 \) and 1040-SR filers: Enter the total of the amounts from Form 1040 or 1040-SR, line 27, and Schedule 3 (Form 1040), line 11. 1040-NR filers: Enter the amount from Schedule 3 (Form 1040), line 11. 25 Subtract line 24 from line 23 . If zero or less, enter \( -0 \) - 26 Enter the larger of line 20 or line 25. Next, enter the smaller of line 17 or line 26 on line 27. Part II-C Additional Child Tax Credit \begin{tabular}{cc|c|c} 27 & This is your additional child tax credit. Enter this amount on Form 1040, 1040-SR, or 1040-NR, line 28 . . & 27 \\ \hline \end{tabular} Schedule 8812 (Form 1040) 2022

\begin{tabular}{l|c|c} Form & Qualified Business Income Deduction & OMB No. 1545-2294 \\ \hline Department of the Treasury Internal Pevenue Servoe & Simplified Computation \\ \hline Name(s) shown on return & Attach to your tax return. \\ \hline \end{tabular} Note. You can claim the qualified business income deduction only if you have qualified business income from a qualified trade or business, real estate investment trust dividends, publicly traded partnership income, or a domestic production activities deduction passed through from an agricultural or horticultural cooperative. See instructions. Use this form if your taxable income, before your qualified business income deduction, is at or below \( \$ 164,900 \) (\$164,925 if married filing separately; \( \$ 329,800 \) if married filing jointly), and you aren't a patron of an agricultural or horticultural cooperative.

Form Department of the Treasury Internal Pevenue Senice If line 3 is a loss and: - Line \( 1 d \) is a loss, go to Part II. - Line 2d is a loss (and line \( 1 d \) is zero or more), skip Part II and go to line 10. Caution: If your filing status is married filing separately and you lived with your spouse at any time during the year, do not complete Part II. Instead, go to line 10. Part II Special Allowance for Rental Real Estate Activities With Active Participation Note: Enter all numbers in Part II as positive amounts. See instructions for an example.

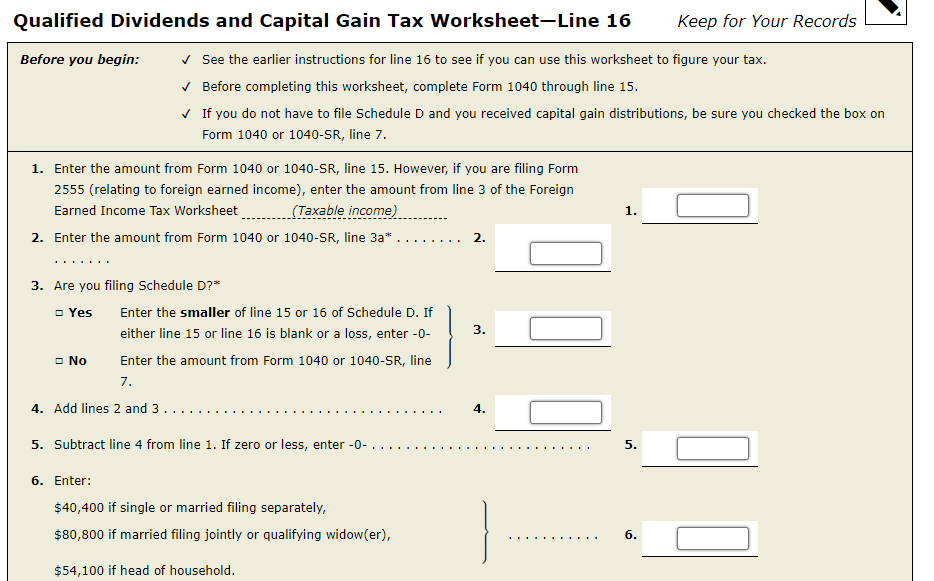

Before you begin: \( \quad \checkmark \) See the earlier instructions for line 16 to see if you can use this worksheet to figure your tax. \( \checkmark \) Before completing this worksheet, complete Form 1040 through line 15. \( \checkmark \) If you do not have to file Schedule D and you received capital gain distributions, be sure you checked the box on Form 1040 or \( 1040-5 R \), line 7. 1. Enter the amount from Form 1040 or \( 1040-S R \), line 15 . However, if you are filing Form 2555 (relating to foreign earned income), enter the amount from line 3 of the Foreign Earned Income Tax Worksheet (Taxable income) 1. 2. Enter the amount from Form 1040 or \( 1040-S R \), line \( 3 a^{*} \ldots \ldots \). 3. Are you filing Schedule D?* \( \left.\begin{array}{l}\square \text { Yes Enter the smaller of line } 15 \text { or } 16 \text { of Schedule D. If } \\ \text { either line } 15 \text { or line } 16 \text { is blank or a loss, enter }-0 \text { - } \\ \square \text { No Enter the amount from Form } 1040 \text { or } 1040-S R \text {, line }\end{array}\right\} \) 3. 7. 4. 5. Subtract line 4 from line 1 . If zero or less, enter \( -0 . \ldots \ldots \ldots \ldots \ldots \ldots \ldots \ldots \ldots \ldots \). 6. Enter: \( \$ 40,400 \) if single or married filing separately, \( \$ 80,800 \) if married filing jointly or qualifying widow(er), \( \$ 54,100 \) if head of household.

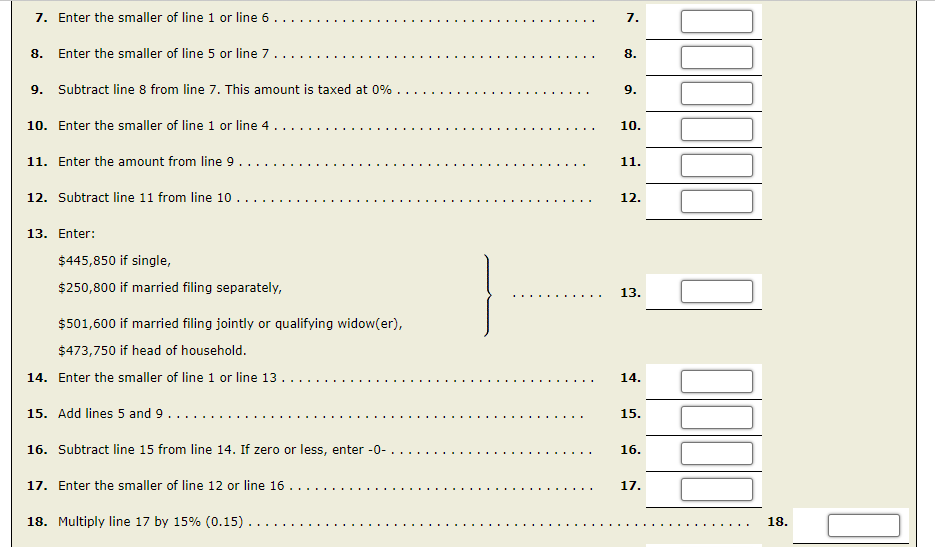

13. Enter: \( \left.\begin{array}{l}\$ 445,850 \text { if single, } \\ \$ 250,800 \text { if married filing separately, } \\ \$ 501,600 \text { if married filing jointly or qualifying widow(er), }\end{array}\right\} \ldots 13 \). \( \$ 473,750 \) if head of household. 16. Subtract line 15 from line 14 . If zero or less, enter \( -0, \ldots \ldots \ldots \ldots \ldots \ldots \ldots \ldots \ldots \) 16.

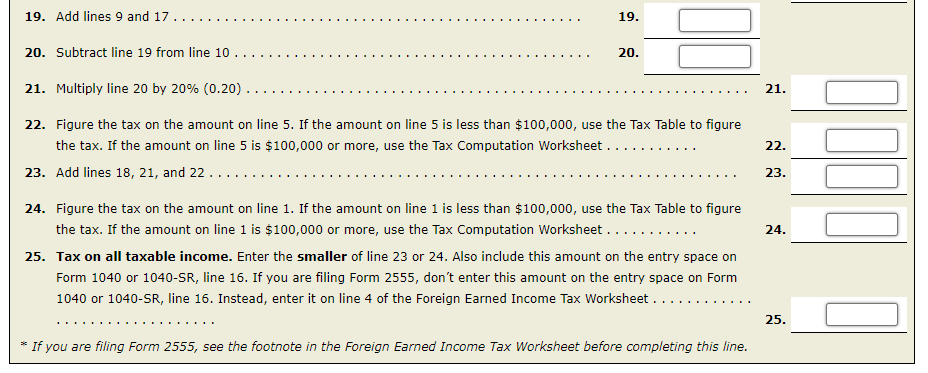

22. Figure the tax on the amount on line 5. If the amount on line 5 is less than \( \$ 100,000 \), use the Tax Table to figure the tax. If the amount on line 5 is \( \$ 100,000 \) or more, use the Tax Computation Worksheet . . . .... . 22. 24. Figure the tax on the amount on line 1 . If the amount on line 1 is less than \( \$ 100,000 \), use the Tax Table to figure the tax. If the amount on line 1 is \( \$ 100,000 \) or more, use the Tax Computation Worksheet . . . . . . . 24. 25. Tax on all taxable income. Enter the smaller of line 23 or 24 . Also include this amount on the entry space on Form 1040 or 1040-SR, line 16. If you are filing Form 2555, don't enter this amount on the entry space on Form 1040 or \( 1040-S R \), line 16 . Instead, enter it on line 4 of the Foreign Earned Income Tax Worksheet . . . . ..... \[ \ldots \ldots \ldots \ldots \] 25. * If you are filing Form 2555, see the footnote in the Foreign Earned Income Tax Worksheet before completing this line.

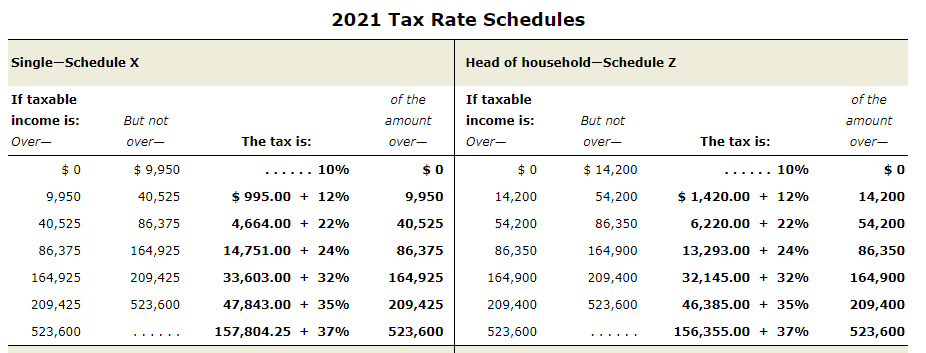

2021 Tax Rate Schedules