Home /

Expert Answers /

Accounting /

note-please-fill-in-the-t-account-as-per-attached-image-and-include-necessary-workings-lisburn-pl-pa679

(Solved): Note: Please fill in the T-account as per attached image and include necessary workings Lisburn Pl ...

Note: Please fill in the T-account as per attached image and include necessary workings

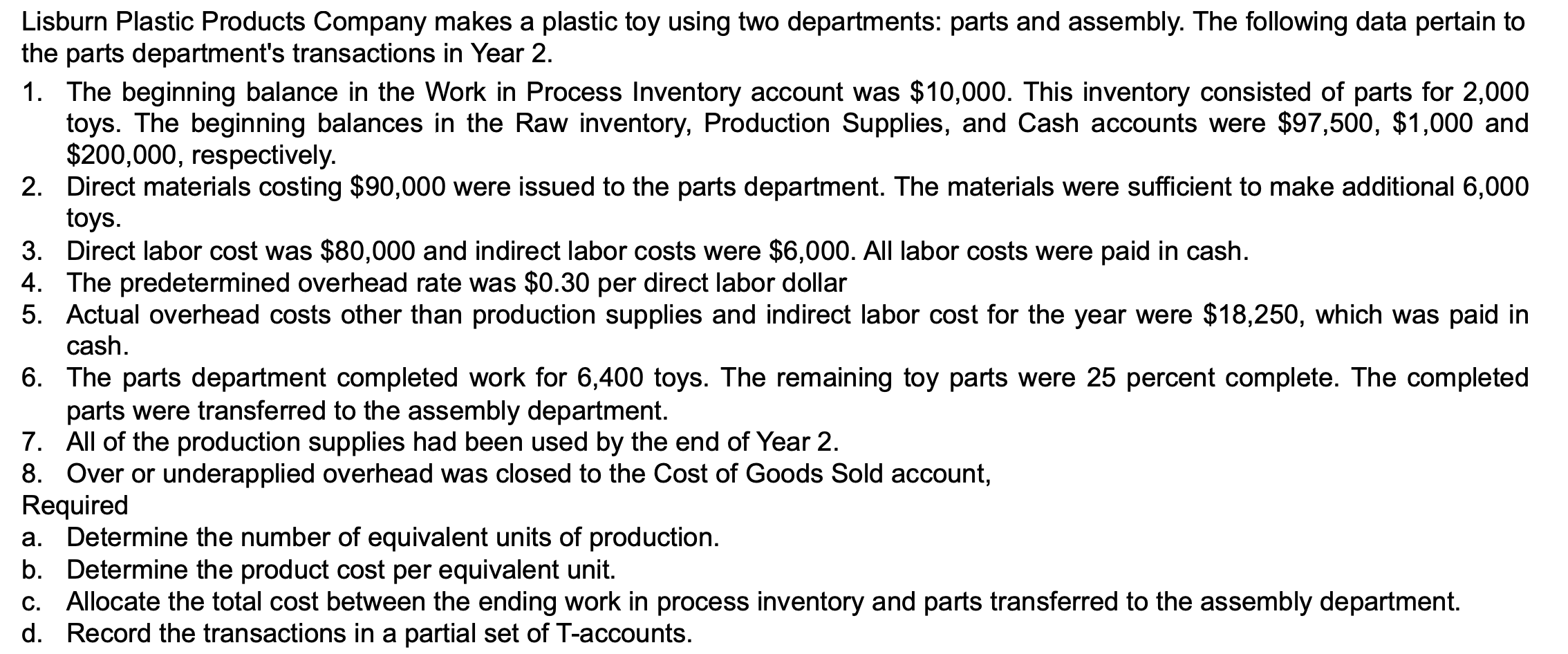

Lisburn Plastic Products Company makes a plastic toy using two departments: parts and assembly. The following data pertain to the parts department's transactions in Year \( 2 . \) 1. The beginning balance in the Work in Process Inventory account was \( \$ 10,000 \). This inventory consisted of parts for 2,000 toys. The beginning balances in the Raw inventory, Production Supplies, and Cash accounts were \( \$ 97,500, \$ 1,000 \) and \( \$ 200,000 \), respectively. 2. Direct materials costing \( \$ 90,000 \) were issued to the parts department. The materials were sufficient to make additional 6,000 toys. 3. Direct labor cost was \( \$ 80,000 \) and indirect labor costs were \( \$ 6,000 \). All labor costs were paid in cash. 4. The predetermined overhead rate was \( \$ 0.30 \) per direct labor dollar 5. Actual overhead costs other than production supplies and indirect labor cost for the year were \( \$ 18,250 \), which was paid in cash. 6. The parts department completed work for 6,400 toys. The remaining toy parts were 25 percent complete. The completed parts were transferred to the assembly department. 7. All of the production supplies had been used by the end of Year 2 . 8. Over or underapplied overhead was closed to the Cost of Goods Sold account, Required a. Determine the number of equivalent units of production. b. Determine the product cost per equivalent unit. c. Allocate the total cost between the ending work in process inventory and parts transferred to the assembly department. d. Record the transactions in a partial set of T-accounts.

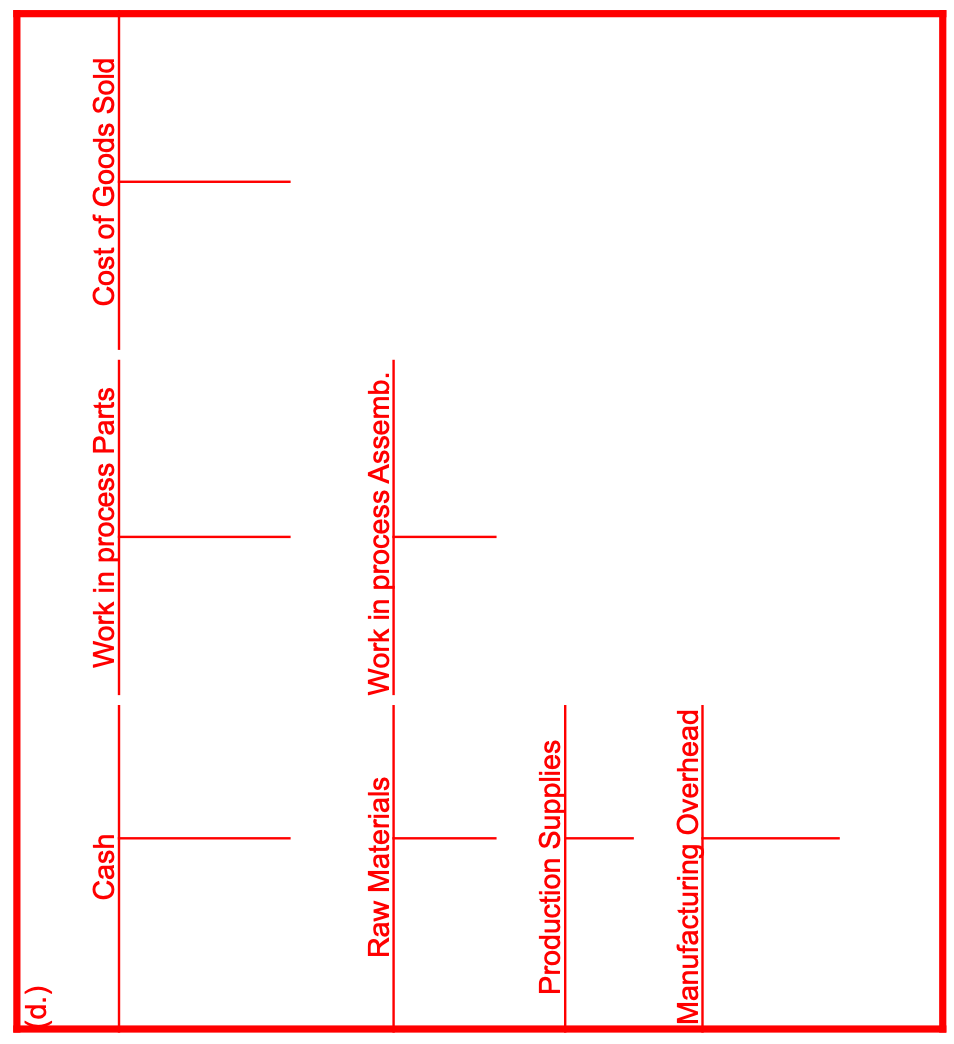

(d.) Raw Materials Work in process Assemb. Production Supplies Manufacturing Overhead

Expert Answer

Solution: a Calculation of number of equivalent units of production = Units completed and transferred + Ending WIP = 6400 + (2000+6000-6400)*25% = 6800 units b Calculation of product cost per equivalent unit = Total Costs / Equivalent units = ( Begin